Credit Rating vs. Credit Score: What’s the Difference?

Understanding the differences between your credit rating and credit score is essential to maintaining good financial health. Your credit score impacts how prospective creditors view you as a borrower, so it’s important to know what these two terms mean – and when each is used.

In this blog post, we will break down what each of these terms means and provide insight into how they work together to influence your overall financial standing.

Credit Rating vs. Credit Score

Your Credit Rating is the overall opinion of your creditworthiness. Credit ratings are used by lenders to assess your ability to repay a loan or line of credit. This rating is compiled from information that creditors and credit bureaus have collected about you over time.

It's important to note that Credit Ratings can vary depending on the lender, as different lenders have different criteria for what constitutes a good Credit Rating.

Your Credit Score, on the other hand, is an algorithm-based estimate of your Credit Rating. Credit scores are derived from information that credit bureaus collect about you and can range anywhere from 300 to 850. The higher your Credit Score, the better your financial standing and the more likely you are to receive good loan offers.

Credit Scores are generally considered a “snapshot” of your Credit Rating, and they allow lenders to quickly assess your Creditworthiness.

What Is a Credit Rating?

Your credit rating is a comprehensive look at your credit history and financial standing. Credit ratings are typically composed of two parts: your payment history, which looks at whether or not you have made payments on time in the past; and an assessment of the amount of money you owe, which can include open lines of credit, student loan debt, etc.

Credit ratings are used to determine your creditworthiness and whether or not you will be approved for a loan. Credit ratings can also help lenders decide how much interest they’ll charge you on the loan.

How Is It Determined?

Credit ratings are determined by looking at your payment history and other factors like the amount of money you owe. Credit ratings are typically assigned by credit bureaus, such as Equifax or TransUnion.

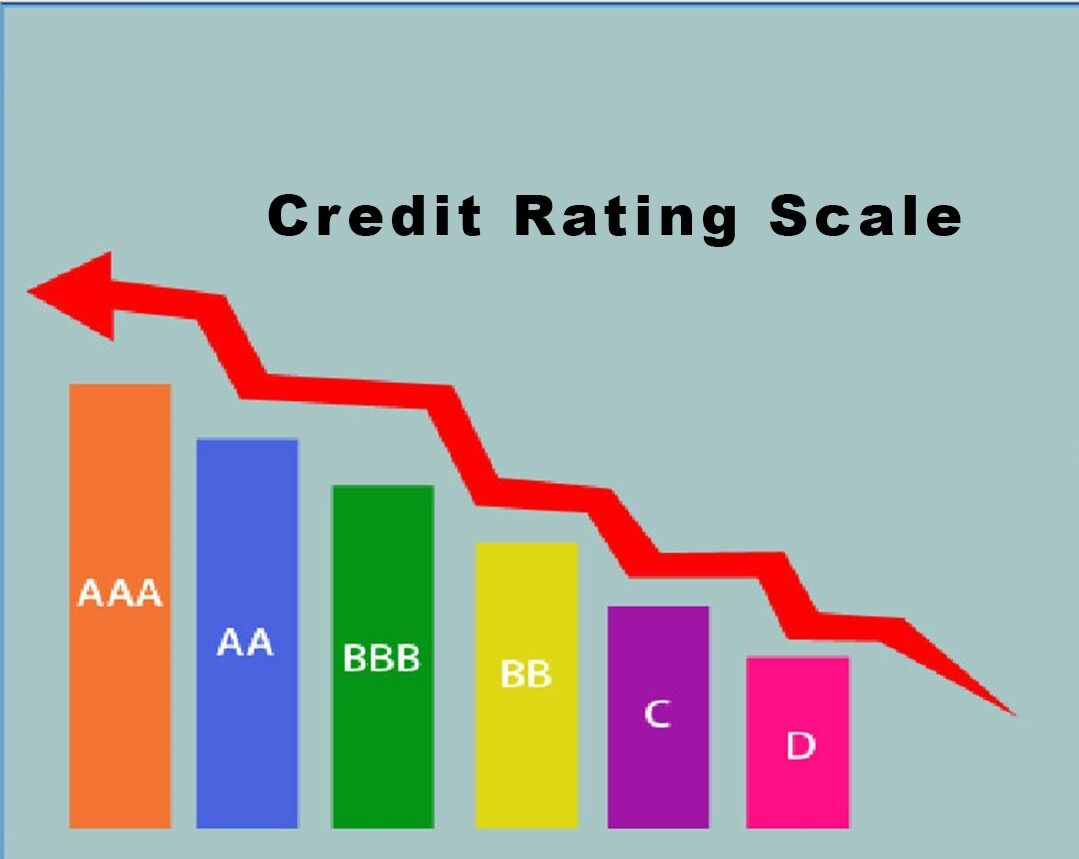

Credit bureaus use complex algorithms to calculate and assign a credit rating based on the information in your credit profile. Credit ratings can also be determined by creditors, such as banks or other lenders. Credit ratings can range from “good” to “poor” and everything in between.

Pros and Cons

pros

Credit ratings provide an accurate assessment of your creditworthiness and can help you get better terms when applying for a loan. Credit ratings are also used by creditors to determine if they should approve your loan application.

cons

Credit ratings are based on information in your credit report, which means they may not always be up-to-date. Credit ratings can also be impacted by inaccurate information in your credit report, which can lead to a lower score.

What Is a Credit Score?

Your credit score is a numerical representation of your creditworthiness and financial standing. Credit scores are typically comprised of five elements: payment history, length of credit history, types of credit used, amount of debt owed, and new credit inquiries.

Credit scores are typically generated by the three major credit bureaus: Experian, Equifax, and TransUnion. Credit scores range from 300 to 850; the higher your score, the more likely it is that you will be approved for a loan or other type of credit.

Credit scores are typically used by lenders to determine your interest rate and other terms of a loan or line of credit.

How Is It Determined?

Credit scores are determined by looking at the five elements listed above: payment history, length of credit history, types of credit used, amount of debt owed, and new credit inquiries. Credit scores are calculated using complex algorithms and the information in your credit profile.

Credit scores are assigned by credit bureaus such as Experian, Equifax, and TransUnion. Credit scores can range from 300 to 850; the higher your score, the better terms you will likely be offered when applying for a loan or line of credit

Pros and Cons

Pros

Credit scores give lenders an accurate assessment of your creditworthiness and can help you get better terms when applying for a loan. Credit scores are also updated regularly, so they are always up-to-date.

Cons

Credit scores can be impacted by inaccurate information in your credit report, which can lead to a lower score. Credit scores may also be lower if you have a limited credit history, as it may be difficult for lenders to accurately assess your risk level. Credit scores are also often used in insurance applications, so they can influence the premiums you pay.

FAQs

What is the difference between rating and score?

The difference between a rating and a score is that a rating is an assessment of your creditworthiness while a score is a numerical representation of your financial standing.

Credit ratings are determined by looking at your payment history and other factors, while credit scores take into account five elements: payment history, length of credit history, types of credit used, amount of debt owed, and new credit inquiries.

Credit ratings are typically assigned by credit bureaus while credit scores are generated by the three major credit bureaus: Experian, Equifax, and TransUnion. Credit ratings range from “good” to “poor” whereas credit scores range from 300 to 850.

What factors influence my credit rating and score?

Your credit rating is determined by factors such as your payment history, length of credit history, types of credit used, amount of debt owed, and new credit inquiries. Credit scores are generated by the three major credit bureaus: Experian, Equifax, and TransUnion.

Credit scores factor in five elements: payment history, length of credit history, types of credit used, amount of debt owed, and new credit inquiries. Credit scores determine your overall financial standing and can impact how prospective lenders view you as a borrower.

How often should I check my score?

It is recommended to check your credit report at least once every 12 months. This will help you stay on top of any inaccurate information in your report, as well as identify any potential signs of identity theft or fraud.

Conclusion

In conclusion, it’s important to recognize the distinction between a credit rating and a credit score. Knowing the difference helps us understand our financial situation better and makes us more empowered decisions when managing our finances.

By being aware of both a rating and a score, we can apply for credit responsibly and understand how lenders use these tools to assess applicants.

On this page

Credit Rating vs. Credit Score What Is a Credit Rating? How Is It Determined? Pros and Cons pros cons What Is a Credit Score? How Is It Determined? Pros and Cons Pros Cons FAQs What is the difference between rating and score? What factors influence my credit rating and score? How often should I check my score? Conclusion

By Kelly Walker : Mar 26, 2023

What Are Best Endeavors?

Do you have big dreams and goals but need to know how to get started? Read our article to learn about the best endeavors, their meaning, and the benefits they bring so you can start progressing toward your success story.

Read More

13944

By Rick Novak : Feb 22, 2023

Taxation of Mutual Funds

You are required to pay taxes when you hold mutual fund shares and when you sell your shares. The primary sources of mutual funds taxes are capital gains (when you sell shares in the fund) and dividends (when you own mutual funds) when you keep funds in taxable accounts.

Read More

2950

By Kelly Walker : Aug 11, 2023

Investment Considerations and Strategies Following a Debt Ceiling Resolution

Observing the financial markets recently would reveal a fascinating dynamic. Explore the best investments for debt ceiling deals in the U.S. in this article.

Read More

12046

By Kelly Walker : Jun 28, 2023

Best Students Credit Cards Of 2023: A Detailed Guide

Get the most out of your college experience by choosing the best student credit cards. We compare and review the top picks so you can make an informed decision.

Read More

19355

By Rick Novak : Jan 28, 2023

What Is a No-Load Fund?

No-load funds are an excellent option for investors looking to diversify their portfolios without paying hefty trading commissions. They offer low costs, a wide range of potential returns and the ability to manage risk and maximize returns through proper research and selection.

Read More

13710

By Kelly Walker : Mar 30, 2023

Financial Planner vs. Financial Advisor: What’s the Difference?

Have you ever wondered about the difference between a financial planner and a financial advisor? Find out here! Learn which type of professional to turn to for help so that you can make informed decisions about your finances.

Read More

16313

By Rick Novak : Feb 04, 2023

Tax Preparer vs. Software: How You Should Choose

You should use caution in selecting the preparer since you will be liable under the law regardless of who prepares your tax return

Read More

641

By Kelly Walker : Jan 28, 2023

Should You Buy a House at Auction?

Purchasing a home through an auction can be a great way to secure a property at a good price. However, there are risks associated with the process that must be taken into account. Before bidding on a property, it is important to research and ensures all paperwork is in order.

Read More

12542

By Kelly Walker : Jun 02, 2023

What Is the Net Working Capital Ratio?

Understanding the net working capital ratio is essential to managing your finances and accurately evaluating investment opportunities. Learn how to calculate it and why it matters with this guide!

Read More

19684

By Kelly Walker : Mar 29, 2023

Review Of The Hilton Honors American Express Card 2023

The Hilton Honors American Express Card is a co-branded credit card that allows cardholders to earn rewards and benefits for their stays at Hilton hotels. In this article, we will cover the various benefits and features of the card, the Hilton Honors Rewards program, how to use the card to maximize rewards, and how it compares to other hotel and travel rewards credit cards.

Read More

9060

By Kelly Walker : Mar 30, 2023

How to Read the Letter Offering You Financial Aid

A student's financial aid eligibility and the amount of aid they will receive are outlined in an award letter. The document details the terms and conditions of several financial aid forms, such as grants, loans, work-study, and scholarships. Making educated decisions about paying for college and avoiding unexpected fees or debt requires a thorough understanding of the information provided in the award letter.

Read More

1752

By Kelly Walker : Feb 04, 2023

Max Life Insurance Review 2023: Everything You Need To Know

Max Life Insurance offers short-term and kid life policies. Although it offers a wide variety of plans, only a subset is accessible to customers outside India.

Read More

18895