What Effect Does Your Credit Score Have On Your Vehicle Insurance?

Feb 07, 2024 By Triston Martin

Good driving habits, getting a safer car and consolidating home and auto coverage are just a few strategies to reduce auto insurance costs. However, not all drivers know that their credit ratings could be a factor in how much they pay for car insurance. If you need another motivation to work on your credit, consider that doing so might result in cheaper monthly payments for auto insurance. Many factors, including driving history, Does Credit Affect Car Insurance, the kind of vehicle used, and the number of incidents in which you were involved, contribute to the cost of auto insurance. Poor credit drivers should expect an average rise in premiums of 76%, according to a review of auto insurance premiums conducted by Forbes Advocate in the 46 states that use credit as a pricing component. That's an increase of almost $1,180 every year on average.

Why Do Auto Insurance Premiums Depend On Credit?

John Espenschied, the founder of Insurance Agents Group and an insurance specialist with over 20 years of experience, says, "Whenever you apply for vehicle insurance, the firm examines your credit rating." You may find it difficult to get coverage if your credit score is poor or if there is evidence that you are spending more than you earn. Car insurance firms utilize your credit score as another risk indicator alongside your driving history. As Adrian Mak, CEO at AdvisorSmith, confirms, "yes," most auto insurers do include credit scores when determining prices. "Additional consideration is given to characteristics like the driver's record, claims record, ZIP code, commercial vehicle, and many more."

What Exactly Are Credit-Based Insurance Ratings?

Many motor insurance firms employ a credit-based insurance score to swiftly and readily detect risk among customers. Insurers use this data to calculate your risk and predict whether or not you will pay your premiums on time or submit a claim. As noted by Espenschied, insurance rates may now be determined based on a person's credit score. "Companies like Fair Isaac Corp. utilize FICO scores, the most popular credit score, to compute premium prices based on insurance, your driving record and risk assessment," says the article.

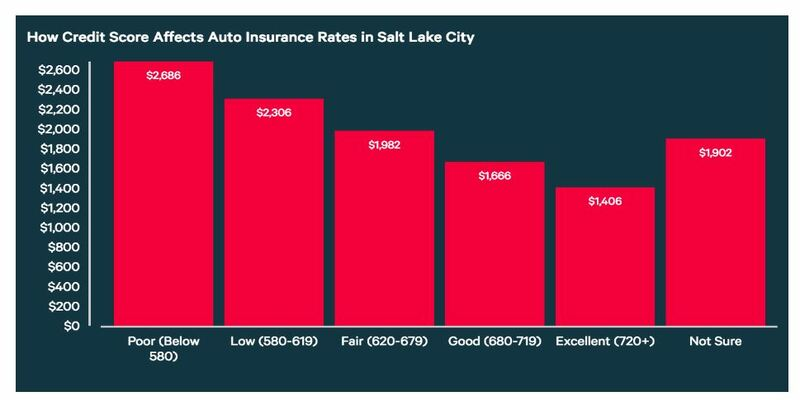

How Much More Will My Vehicle Insurance Cost If My Credit Rating Is Below Average?

Average annual premiums for liability-only coverage in the United States are $565, with comprehensive coverage costing an additional $1,674. Your premium may be much more or cheaper than average based on your credit history and other rating variables. Although this is not legal in certain places, your gender might affect the average cost of car insurance. Due to their higher accident risk, male drivers generally pay more than their female counterparts. Comprehensive insurance premiums for men and women with varying credit scores are shown below.

Average Insurance Costs By State And Credit Score

Most jurisdictions utilize credit history to set insurance premiums, but others don't. The practice of utilizing credit scores as nothing more than a factor for setting auto insurance premiums has been outlawed in California, Hawaii, Pennsylvania, and Michigan. Credit scores aren't used as much in determining vehicle insurance rates in Maryland, Oregon, as well as Utah. Financial institutions' ability to use credit history for setting rates and premiums is restricted by law in these states.

Methods For Raising Your Credit Rating

From overdue invoices to applying for a new loan, there are several ways in which your credit score might take a hit. Credit scores, however, may be changed. Your credit score may be raised via the following means:

Examine Your Credit Report:

One free credit report each year is yours to request. If you check your credit score often, you can see changes that might lead to problems before they escalate.

Make Payments On Time:

A negative mark on your credit record will only grow due to your late payments. If you start establishing a habit of timely payments, it might positively affect your finances over time.

Work On How Much You Use Your Credit:

Having several credit cards at their limits might negatively affect a credit report. The insurance company could start to fear that you can't keep up with your payments because you've taken on too much debt. Paying down debt such that your debt is less than 30% of your income might be advantageous.

Take A Break From Opening New Accounts:

Credit scores might hit the number of hard queries potential lenders make whenever you apply for brand-new credit. Instead of opening new lines of credit, prioritize paying off the ones you already have to reduce your repayment ratio.

Conclusion:

Regular payments, such as those required by subscription services, including insurance, may be easily categorized as fixed costs. However, if you do some research, you can discover a strategy to cut costs that will result in savings immediately and over the next months.

-

Mortgages Oct 18, 2023

Mortgages Oct 18, 2023Things Buyers Should Know About Real Estate Contingencies

Getting started with crypto, NFTs, and other DeFi platforms is easier than you would think. OKX is a trusted platform for buying, selling, and storing digital assets. When you make a deposit of over $50 through a crypto purchase or top-up within 30 days of signing up, you can connect your current wallets and be entered to win up to $10,000. Take the time to read the details and join right now.

-

Mortgages Oct 27, 2023

Mortgages Oct 27, 2023A Guide To Choosing And Purchasing An Electric Vehicle

Purchasing an EV, whether new or used, is a huge step forward. The decision to purchase an electric vehicle (EV) was previously more frightening than now, but new and established automakers are flooding the market with fresh EV alternatives. In the not-too-distant future, drivers may expect to find an electric car that suits their needs.

-

Know-how Dec 07, 2023

Know-how Dec 07, 2023Monetarism Deciphered: A Comprehensive Guide

This document provides a comprehensive overview of monetarism, a school of thought in monetary economics that emphasizes the role of governments in controlling the amount of money in circulation.

-

Know-how Mar 20, 2024

Know-how Mar 20, 2024The 7 Golden Rules for Having More Money for Your Golden Years

Explore the top strategies for enhancing your retirement savings, including starting early, diversifying investments, and cutting costs.